Using Reasonable Expectations to Contest the Household Exclusion In a Car Insurance Policy

Using Reasonable Expectations to Contest the Household Exclusion In a Car Insurance Policy

Insurance companies are the worst. They advertise heavily and tell consumers that they are there to help them. They collect premiums but then refuse to pay fairly when a claim is presented. They do this for one reason—to increase profits.

The sale of insurance is a business. In fact, it is a big business. According to the Insurance Information Institute, the insurance industry net premiums written in 2021 totaled 1.4 trillion. Yes, that is trillion with a “T.”

According to the U.S. Department of Labor, the insurance industry in the United States employed 2.8 million people in 2021. That is more than the populations of 15 states including Nebraska and New Mexico.

Auto Insurance Companies are For Profit Businesses

Most insurance companies are publicly traded corporations. Progressive is the largest commercial auto insurer in the United States. It is publicly traded on the New York Stock Exchange. Its ticker symbol is PGR.

Its competitors are publicly traded as well. This includes Allstate (ALL) and Travelers (TRV) among several others.

Since these companies are publicly traded, increasing profits is a primary goal. Like all companies, profits and losses drive stock share prices. As a result, the more profitable these companies are, the more wealth they can deliver to their stockholders including the CEOs that hold those stock shares.

An easy way for an insurance company to increase profits is by collecting premiums and not paying claims. The more that an insurance company has to pay out in claims, the more it affects their bottom line. As a result, insurance companies, and those working for them, have a huge incentive to deny claims whenever they can. Indeed, they regularly do.

No One Reads Their Car Insurance Policy

No one ever reads their car insurance policy when signing up for insurance. Typically, a person tells an insurance agent or broker what general coverage they want. The agent or broker, who are essentially salespeople, may make suggestions and explain coverages in general terms. However, they do not go over in any detail what the policies actually set forth.

In reality, these sales agents likely have no clue what is contained in the policies they sell. Specifically, they have never read those policies closely. Even if they did, they likely would not understand them.

However, they do not go over in any detail what the policies actually set forth.

A person may never even receive their actual insurance policy. They may get a summary or a declaration page, but they seldom get the insurance policy contract itself. What is certain, is that no one ever gets their insurance policy before they agree to the coverage.

An insurance policy is a contract for insurance. A person buys insurance with no idea as to exactly what it covers. In short, a person agrees to a contract without even really knowing the terms of it.

Car Insurance Policies Are Complicated Contracts

Insurance policies are complicated contracts. They have definitions, terms, exclusions, addendums and more. Several of the provisions in these contracts must be interpreted by applying definitions set forth in other areas of the contract. Many of these provisions must be read in conjunction with each other.

These insurance contracts are often difficult for even attorneys to understand. Even if an attorney believes that he understands the insurance provisions, often times other attorneys will have different interpretations of those exact same provisions. As a result, there are legal cases and court rulings that specifically decide the interpretation of insurance contract provisions. These cases not only rule on what the meaning of the provision is, but also on whether the provision is legal and how it should be applied.

The Average Person Can Not Understand Their Car Insurance Policy

If attorneys are unable to agree on these insurance contract provisions, how is the regular consumer supposed to? The answer is they can’t. The average person is not expected to understand their car insurance policy and all the applications of it.

The insurance companies know this. They spend tens of millions of dollars hiring high-price lawyers to draft their insurance policies to favor them. It is essentially a unilateral contract where the consumer has little to no bargaining power.

The Exclusions Contained in Car Insurance Policies

Whenever they can, insurance companies include language in their policies to limit their liability. Specifically, they include complicated provisions that exclude coverage. These exclusions look to protect the insurance companies from having to pay out on claims. Often times, they exclude the claims most likely to occur.

One such claim is that of a family member who is involved in a crash in which another family member from the same household is driving and found at fault. Naturally, that situation occurs frequently. For example, when a husband and wife are together or parent and their children.

The Family Member Household Exclusion

Most insurance policies have a family member, household exclusion which limits an injured family member’s ability to recover from their own household family member if he or she is at fault. In other words, if a father is at fault for causing a car crash in which his children are injured, his injured children would not be able to recover from the insurance company the full amount of his liability insurance.

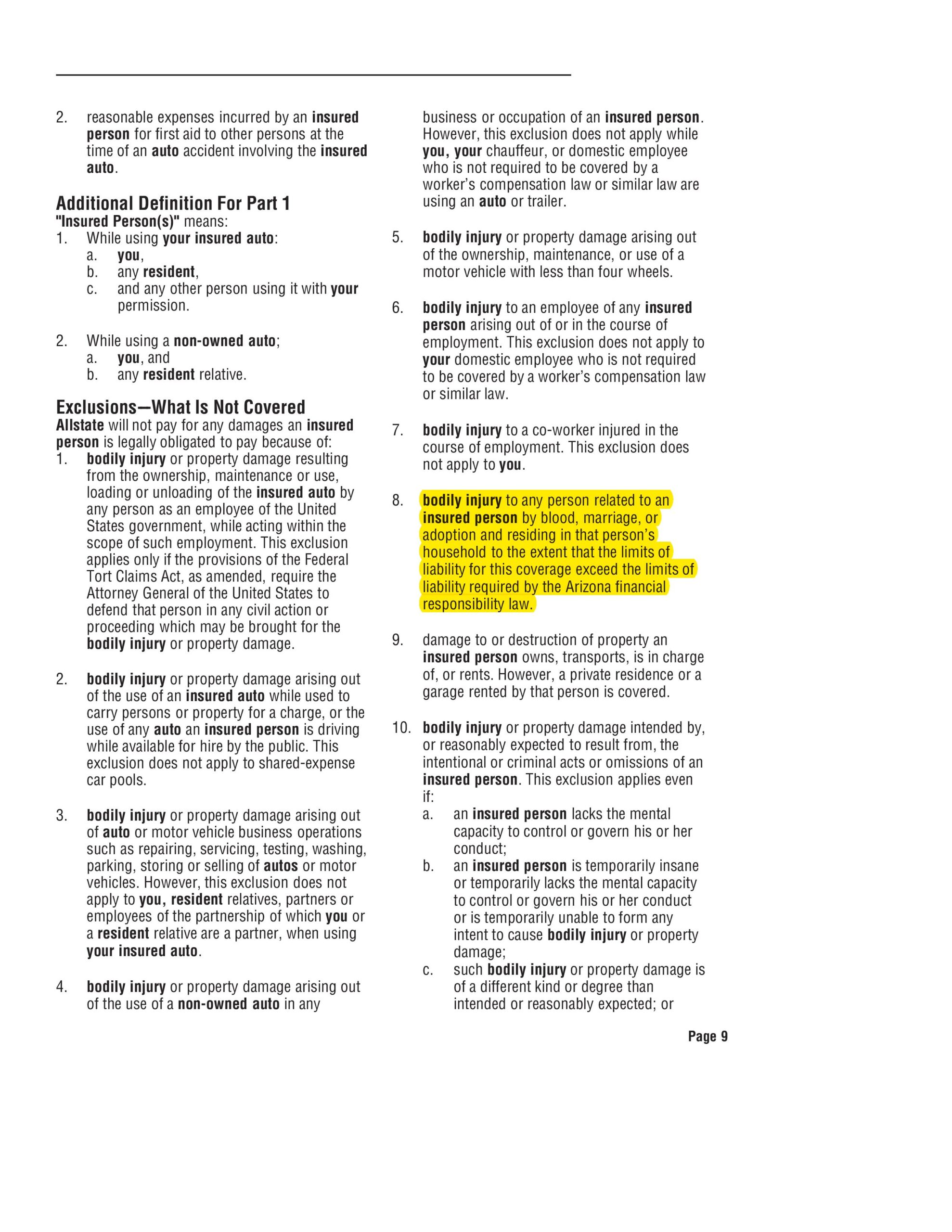

The exclusion is usually couched between others in an exclusion section. The provision usually is something like the following which was taken from an Allstate policy:

Allstate will not pay for any damages an insured person is legally obligated to pay because of… 8. bodily injury to any person related to an insured person by blood, marriage or adoption and residing in that person’s household to the extent that the limits of liability for this coverage exceed the limits of liability required by Arizona financial responsibility law.

Of course, the average person has no idea what this means, much less would even be able to locate this provision in the approximately twenty page car insurance contract. The average person has no idea what is meant by “the limits of liability required by Arizona financial responsibility law.” What this provision actually means, is that in no situation will the insurance company pay more than what the state minimum automobile insurance limits are to a family member. That amount is currently $25,000.

The Family Member Household Exclusion Applied

The following illustrates this concept. Assume a couple obtains $100,000 in automobile insurance liability coverage. Liability coverage then applies when either one of them causes a crash and injures someone as a result.

This coverage would apply to other random drivers on the road who were injured. It would also apply to any passengers in the car who were injured, except for family members living in the same household. It would apply to any friends riding in the vehicle. It would apply to their brothers or sisters who may be visiting over the holidays and riding in their car. It would apply to adult children who moved out to go to college and were back visiting. In any of those circumstances, the full $100,000 in liability coverage would be available to the injured person.

The Exclusion Financially Benefits the Insurance Companies

However, the coverage does not apply to the people who are the most important. Those are the household family members that are riding in the vehicle every day. All that is available for their injuries is $25,000. In other words, everyone else is more protected than the people that matter most.

In other words, everyone else is more protected than the people that matter most.

It is also no coincidence that the excluded household family members are also the ones most likely to be injured. They are the ones who will be riding as passengers in the vehicles the most. They are also the ones most likely to have a claim for injuries. By excluding them, the insurance companies know that they are significantly reducing their exposure to one of the most common claims that could arise.

What is the Reasonable Expectations Doctrine?

The reasonable expectations doctrine is a court-created application of law that invalidates parts of in insurance policy contracts when those parts defy the reasonable expectations of a purchasing consumer. In sum, it makes unenforceable standardized terms in insurance contracts if those terms are not within the reasonable expectations of a consumer. In discussing reasonable expectations, the Arizona Supreme Court has stated that “an insurance company should not take advantage of the average consumer by appearing to promise certain coverage, and then eviscerating that coverage with buried fine print.”

…an insurance company should not take advantage of the average consumer by appearing to promise certain coverage, and then eviscerating that coverage with buried fine print.

The first case to apply reasonable expectations to auto insurance policies was Darner Motor Sales, Inc. v. Universal Underwriters Ins. Co. In Darner, the court adopted the application of the reasonable expectations doctrine. Although in Darner, there were allegations of express misrepresentations by the insurer. In later cases, the doctrine was applied even without any misrepresentations.

The Reasonable Expectations Doctrine Has Been Applied to Invalidate the Household Exclusion

There are several cases where the reasonable expectations doctrine has been applied to invalidate the household exclusion. One such case is Do by Minker v. Farmers Insurance Company of Arizona. In that case, a father purchased car insurance and later caused a single car accident where he was driving and his minor children were injured.

Farmers sought to use the household exclusion to limit the coverage for the children to the state minimum which was $15,000 per person at the time. This is despite the father having obtained $50,000 in coverage per person under the policy. The appellate court upheld a decision that the household exclusion was unenforceable thus allowing $50,000 in coverage per child.

However, in that case, the father testified that he wanted his children to all be covered up to the $50,000 per person maximum. The father testified that he was told by an insurance agent that if his family were hurt they could recover that amount. Further, he testified that he believed that the coverages available for his children were the same as held out on the insurance declarations page.

The Application of the Reasonable Expectations Doctrine is Fact Specific

The cases that have held that reasonable expectations can invalidate the household exclusion are fact specific. In other words, there is no case that states that the household exclusion is illegal or void as a matter of law. To the contrary, the household exclusion is very much a legal contract provision. However, whether or not it can be enforced must be analyzed on a case-by-case basis.

Most attorneys are not familiar with the reasonable expectations doctrine. Even less have argued or litigated it. As such, if you are seeking to use it, it is important you consult with a skilled attorney who is up to speed on its application.

The attorneys at Scottsdale Injury Lawyers are. We have argued the reasonable expectations doctrine in various insurance coverage disputes. We have used it to successfully recover seven figure results for our clients.

Reasonable Expectations Has Been Applied to Other Insurance Policy Exclusions

The reasonable expectations doctrine has been used to stop the enforcement of other exclusions in car insurance policies. It has been used to defeat a “resident relative” exclusion. It has also been used to stop the enforcement of a “named insured” exclusion. Further, it has been used to stop the enforcement of exclusions in umbrella policies as well.

Contact Scottsdale Injury Lawyers Today to Discuss Your Car Accident Case

If you were involved in a car accident and are being taken advantage of by an insurance company, contact Scottsdale Injury Lawyers today. Our car accident attorneys will fight to make sure you are treated fairly. We know the law and cases that require the insurance companies to come to the table. A consultation is free and we only earn a fee if we recover for you.

About the author: The content on this page was provided by Scottsdale personal injury attorney and civil rights lawyer Tony Piccuta. Piccuta graduated with honors from Indiana University-Maurer School of Law in Bloomington, Indiana (Previously Ranked Top 35 US News & World Report). Piccuta took and passed the State bars of Arizona, California, Illinois and Nevada (all on the first try). He actively practices throughout Arizona and California. He is a trial attorney that regularly handles serious personal injury cases and civil rights lawsuits. He has obtained six and seven figure verdicts in both state and federal court. He has been recognized by Super Lawyers for six years straight. He is a member of the Arizona Association of Justice, Maricopa County Bar Association, Scottsdale Bar Association, American Association for Justice, National Police Accountability Project and Consumer Attorneys of California, among other organizations.

Disclaimer: The information on this web site is for informational purposes only and does not constitute legal advice. The information on this page is attorney advertising. Reading and relying upon the content on this page does not create an attorney-client relationship. If you are seeking legal advice, you should contact our law firm for a free consultation and to discuss your specific case and issues.

References: