SIL Turns Denial of Car Accident Claim Into $100,000 Settlement

SIL Turns Denial of Car Accident Claim Into $100,000 Settlement

The car accident attorneys at Scottsdale Injury Lawyers have achieved another six-figure result. Our attorneys recently settled a case for $100,000 for a client who was a pedestrian when he was struck by a car. The work performed by our injury attorneys was particularly impressive because the insurance company initially denied the claim.

The client was jogging when he was hit by a truck in a crossing area of a sidewalk. The driver of the truck offered to transport the client to a nearby hospital and did so. After dropping the client off, the driver fled the scene and could not be located.

Our attorneys advanced an uninsured motorist claim for the client under his own car insurance policy. The insurance company was State Farm. State Farm denied the claim arguing that coverage was excluded under the insurance agreement. Our attorneys got to work and were able to get State Farm to cover the claim after arguing contract principles and case law.

More About the Car Versus Pedestrian Injury Accident

On April 13, 2023, at approximately 4:00 PM, the client was a pedestrian crossing the crosswalk near the entrance of Thompson Peak Park on Thompson Peak Parkway in Scottsdale, Arizona. On that date and time, the at-fault driver, was operating a pickup truck traveling near the entrance of the park. As the client was crossing the crosswalk, the driver struck the client and seriously injured him.

The client was taken to the emergency room, just down the street, by the driver of the truck. The driver helped him into a wheelchair and then abruptly left without the client realizing it. As a result, the client was unable to obtain the driver’s contact or insurance information.

Police were called to the scene and confirmed this version of events as it was captured on the hospital’s surveillance system. However, the license plate number from the truck was unreadable on the surveillance video. As a result, the client was unable to make a claim under the driver’s insurance as he left the scene without providing his information. Police were also not able to locate and identify the fleeing driver.

The Impact Caused by the Truck

At the time of the collision, the client was not expecting the impact and was unable to brace for it. When the at-fault driver struck him, he was forcefully impacted by the truck. The truck knocked him to the ground where he sustained a second impact and landed on the left side of his body and hit his head. The client was unable to withstand the forces from the impacts without sustaining injury.

The Injuries Sustained by the Client and Initial Treatment

The client presented to an emergency room doctor at the hospital. The doctor noted the client’s complaints of pain in his back and left wrist/forearm. Due to the severity of the client’s symptoms, the doctor ordered CT scans of his chest, abdomen, pelvis, thoracic spine, lumbar spine, cervical spine and brain. The doctor also ordered x-rays of the client’s left hand and left forearm.

The client was diagnosed with the following at the emergency room.

- Closed fracture of one rib of left side

- Contusion of left hip and thigh

- Contusion of finger of left hand

- Probable fracture of distal radius

The client’s injured arm was placed in a soft splint. He was prescribed pain medication. The client was discharged with instructions to follow up for additional medical treatment as needed.

The Broken Arm Was Evaluated Further

The client was a veteran and followed up with the VA Medical Center. There, they diagnosed him with a transection facture nonunion of the top of the ulnar styloid. The ulna is one of the two bones in a person’s forearm. The styloid is the section of the bone near the end where it meets the wrist and hand. In other words, a piece of the end of the client’s lower arm bone near the head broke off.

Fall Injuries Can Result in Fractured Bones

The client likely fractured his ulna when he extended his hand to break his fall. When someone bends their hand back to brace themselves for an impact with the ground, the impact can transfer force to the arm bones. When this occurs, the bones can break.

The Continued Medical Treatment

The client was referred to see a hand specialist. He was also referred to physical therapy. The client participated in physical therapy where he underwent treatment for his back, arm and hip. The client experienced pain in his left hip after the crash. This was caused by his hip making contact with the ground after he was struck by the truck.

The client’s physical therapy sessions lasted more than eight weeks. The physical therapy sessions consisted of the following treatment.

- manual therapy

- therapeutic exercise

- neuromuscular re-education

- canalith repositioning procedures

- gait training

- cupping

- dry needling

- application of hot/cold packs

The physical therapy improved the client’s back and hip problems. However, it did not provide significant relief with respect to the client’s arm injury.

The client underwent additional diagnostic testing of his fractured arm. He also met with an orthopedic surgeon who specialized in wrist and forearm injuries. It was decided that the client would continue to treat conservatively and then consider surgery for his broken arm if his condition deteriorated further.

The Uninsured Motorist Coverage in the Client’s Insurance Policy

The client had uninsured motorist coverage through the policy that he and his fiancé obtained. The policy was in the name of his fiancé and he was added as an additional driver to the policy. His vehicle was also added. Title to his vehicle was held in both he and his fiancé’s name.

What Is Uninsured Motorist Coverage?

Uninsured motorist coverage is an optional coverage that a person can select when they obtain car insurance. Unlike liability coverage, a person is not legally required to have uninsured motorist coverage. However, insurance companies are legally obligated to offer it to customers who purchase automobile insurance.

Uninsured motorist coverage applies when a person is injured and the person who is responsible for contributing to the injuries does not have insurance.

Uninsured motorist coverage applies when a person is injured and the person who is responsible for contributing to the injuries does not have insurance. In that situation, someone with uninsured motorist coverage may collect those benefits. Those benefits are payable by that person’s own insurance company under this optional coverage.

Does Uninsured Motorist Insurance Apply When A Person is a Pedestrian and Not Driving?

Under most policies, uninsured motorist coverage applies even when someone is not driving. Most people do not realize that their automobile insurance may protect them even when they are not using their vehicles. However, both uninsured motorist and underinsured motorist coverage usually applies when someone is hit by a vehicle as a pedestrian or while operating a non-motorized transportation device.

This may include the following:

- When someone is walking

- When someone is running

- When someone is standing

- When someone is riding a traditional bicycle

- When someone is riding a non-powered scooter

- When someone is riding a skateboard

There are exclusions to every insurance policy and the coverages within them. For example, a typical exclusion that applies to uninsured motorist coverage is when the operator of the vehicle is a family member. Insurance policies and their exclusions are sophisticated contracts. As such, it is important to have a highly qualified attorney review your insurance policy to determine what coverages apply and which benefits you may be entitled to.

We Presented an Uninsured Motorist Claim to State Farm

Upon being hired, we presented an uninsured motorist claim to State Farm under our own client’s insurance policy. The claim sought to recover the payment of benefits for our client’s injuries. This included payment for his medical expenses, pain, suffering and disability.

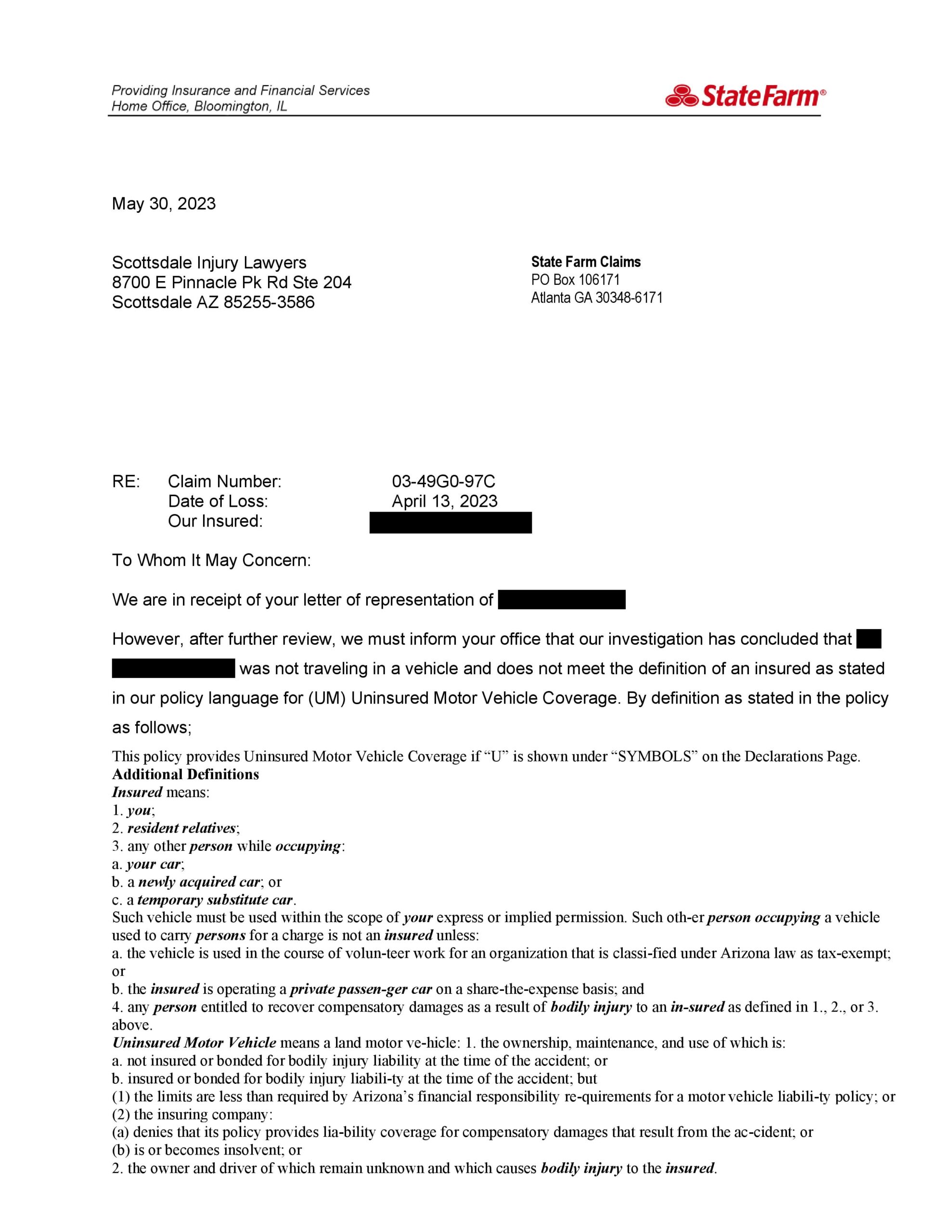

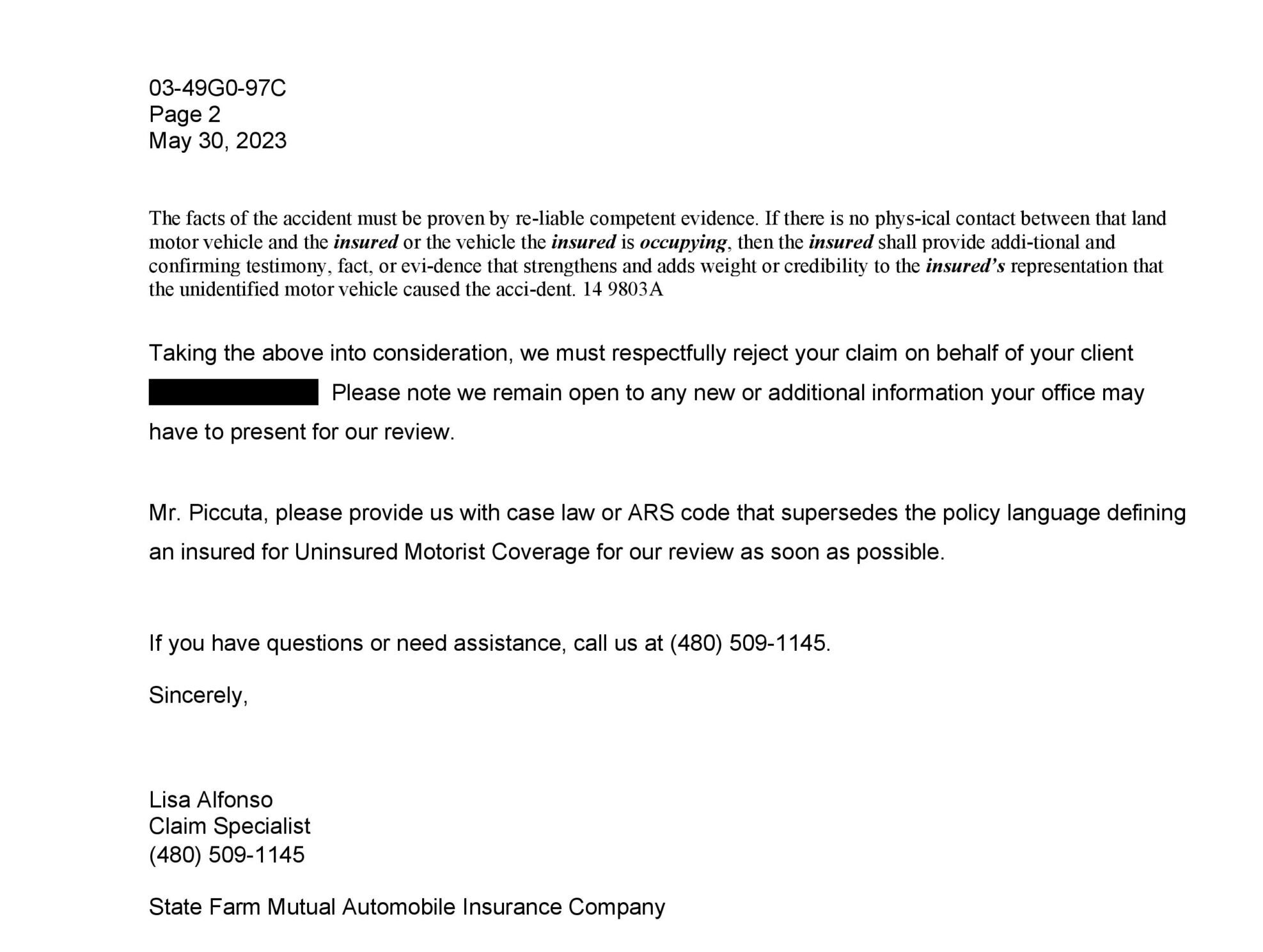

The Insurance Company Wrongfully Denied the Claim

In response to our claim, we received a letter from State Farm stating it was denying the claim. State Farm concluded that our client was added to the policy as an additional driver, not as a named “insured.” As a result, State Farm concluded that our client was not entitled to certain benefits under the policy. One of the benefits from which State Farm claimed he was excluded was uninsured motorist coverage.

Images of the denial letter from State Farm appear below.

We Fought the Insurance Company’s Denial of Coverage

Our experienced personal injury attorneys fought State Farm’s denial. We authored a five-page letter with a factual history of how the insurance policy was obtained and how our client was added to it. A portion of the letter is set forth below verbatim:

Our Office Argued that the Denial Violated Our Client’s Reasonable Expectations

Our office further asserted that the exclusion violated the reasonable expectations of the client. We argued that even if State Farm could make an argument that it did not negligently or fraudulently add our client to the policy as less than an “insured,” the exclusion State Farm relied upon would still be unenforceable. We explained that it was well-established that such exclusions are routinely held unenforceable. That is because such exclusions violate the reasonable expectations of the customer.

We explained that it has long been established under Arizona law, that exclusions, such as the one State Farm was relying on, are unenforceable. We then noted a long line of cases holding that boilerplate exclusions, couched in insurance policy language, are unenforceable as they violate a customer’s reasonable expectations. These cases date back more than 35 years.

The Long Line of Arizona Cases Holding Insurance Policy Exclusions Invalid

Our experienced injury attorneys also set forth the case law that supported extending coverage to our client. We explained that Arizona courts have repeatedly refused to enforce boilerplate insurance policy exclusions. We then cited the following cases:

- Darner Motor Sales, Inc. v. Universal Underwriters Ins. Co., 140 Ariz. 383 (1984). The Arizona Supreme Court held that it would not enforce even unambiguous provisions in standardized insurance contracts which are either contrary to oral representations which had been made with regard to coverage, or which eliminate the dominant purpose of the transaction.

- Gordinier v. Aetna Cas. & Sur. Co., 154 Ariz. 266 (1987). The Arizona Supreme Court enumerated four situations where courts were not required to enforce unambiguous boilerplate terms in insurance contracts. 1) cannot be understood by a reasonable consumer; 2) no notice and the insurance provision is unexpected; 3) conduct of the insurer would make consumers believe they were covered; 4) activity of the insurer induced the insured.

- State Farm Mut. Auto Ins. Co. v. Dimmer, 160 Ariz. 453 (App. 1988). The court held that a household exclusion was unenforceable after applying reasonable expectations doctrine, even absent proof of promises or misrepresentations by insurance agent, because the exclusion was based on technical wording and placed in the policy’s boilerplate and gutted the coverage ostensibly granted by the declarations page.

- Do v. Farmers Insurance Company, 171 Ariz. 113 (1991). The court held that the automobile policy’s household exclusion, providing that coverage did not apply when any family member of insured residing in same household was injured, violated reasonable expectations of insured and was unenforceable.

- State Farm Mut. Auto Ins. Co. v Falness, 39 F.3d 966 (1994). The court held that the reasonable expectations doctrine made named insured exclusion unenforceable as to the passenger spouse who was both a named insured and member of the household.

- Pruett v. Farmers Ins. Co. of Arizona, 175 Ariz. 447 (1993). The court held that an insurance company was not insulated from bad faith liability when relying on a household exclusion that limited payment to the minimum state financial responsibility in light of the insured’s reliance on the reasonable expectations doctrine which made the enforceability a question of fact.

- Morgan v. American Family Mutual Insurance Company, 336 Fed.Appx. 644 (2009). The court held that a named-insured exclusion in an umbrella policy was invalid and unenforceable and that the exclusion ran afoul of Arizona’s reasonable expectations doctrine.

- Jacobson v. American Family Insurance Company, 2020 WL 919173. The court held that the enforceability of an insurance exclusion, which held that relatives that owned their own vehicles were not relatives for UIM coverage purposes, was a question of fact for trial due to reasonable expectations doctrine.

Our letter was sent to State Farm on August 4, 2023. Our letter threatened State Farm with a bad faith insurance claim if they wrongfully denied coverage.

The Insurance Company Extended Coverage

On August 28, 2023, twenty-four days after sending our letter, State Farm sent a letter agreeing to coverage. The letter stated as follows:

“This letter is to advise that State Farm Mutual Automobile Insurance Company has resolved the coverage question(s) stated in my correspondence dated May 15, 2023. This letter is to advise you that the coverage question mentioned in our May 15, 2023 letter has been resolved and we are extending uninsured motorist coverage for your client.”

Do Not Trust Your Insurance Company If Your Claim Is Denied Under An Exclusion

Without an attorney, the client would have believed that State Farm rightfully denied his claim. After all, the language in the policy supported that he was not covered. Of course, State Farm and all their attorneys would not tell him what the law holds and how it could help him. That takes a very skilled and experienced attorney.

It takes a real attorney who handles hard cases and has experience with difficult legal issues. It takes an attorney who is capable of high-level legal research and case analysis. It takes an attorney who is willing to dedicate his or her time and not simply pluck the low hanging fruit. It takes much more than an attorney who merely dances on television and plasters his face on buses and billboards.

The attorneys at our firm do the hard work. We fight the battles other attorneys will not or cannot. Simply put, we are more capable than most personal injury attorneys and we win when other attorneys would not even try.

We Obtained the Full $100,000 Policy Limits for Our Client

After we forced the insurance company to extend coverage, we presented the full scope of our client’s injury claim. We provided the insurance company with evidence supporting how the injury occurred and the medical treatment required. This included the police report, photographs, witness statements, medical records and bills. Earlier this month, the insurance company agreed to pay our client the full $100,000 available under the uninsured motorist policy.

The insurance company agreed to pay our client the full $100,000 available under the uninsured motorist policy.

The Client Appreciated the Hard Work We Put In

The client came to our office several times during the time we handled his case. Each time, he was able to meet with the injury attorney handling his case and discussed it with him face to face. The client knew about the claim denial and the work that we were performing in an effort to obtain coverage. The client was on an emotional roller coaster throughout the process.

The client sent an email to our office after receiving his check. His email stated as follows: “I received my check Tony. I don’t have any words. Thank you so much for everything.”

Contact an Experienced Injury Attorney if You Have a Car Accident Insurance Claim

If you or a loved one was injured in any accident involving a car, truck or other automobile, contact our office today. A highly skilled and experienced lawyer is available now to discuss your case. A consultation is free and we only earn a fee if we recover for you. It costs nothing to call. Call us today at (480) 900-7390.

About the author: The content on this page was provided by Scottsdale personal injury attorney and civil rights lawyer Tony Piccuta. Piccuta graduated with honors from Indiana University-Maurer School of Law in Bloomington, Indiana (Previously Ranked Top 35 US News & World Report). Piccuta took and passed the State bars of Arizona, California, Illinois and Nevada (all on the first try). He actively practices throughout Arizona and California. He is a trial attorney that regularly handles serious personal injury cases and civil rights lawsuits. He has obtained six and seven figure verdicts in both state and federal court. He has been recognized by Super Lawyers for six years straight. He is a member of the Arizona Association of Justice, Maricopa County Bar Association, Scottsdale Bar Association, American Association for Justice, National Police Accountability Project and Consumer Attorneys of California, among other organizations.

Disclaimer: The information on this web site is for informational purposes only and does not constitute legal advice. The information on this page is attorney advertising. Reading and relying upon the content on this page does not create an attorney-client relationship. If you are seeking legal advice, you should contact our law firm for a free consultation and to discuss your specific case and issues.

References:

[1] https://scholar.google.com/scholar_case?case=10362639319847898959&q=140+Ariz.+383+&hl=en&as_sdt=4,3

[3] https://scholar.google.com/scholar_case?case=8612641686793912695&q=160+Ariz.+453+&hl=en&as_sdt=4,3

[4] https://scholar.google.com/scholar_case?case=10042126020501647877&q=171+Ariz.+113&hl=en&as_sdt=4,3

[5] https://scholar.google.com/scholar_case?case=621214870701339771&q=39+F.3d+966&hl=en&as_sdt=803

[6] https://scholar.google.com/scholar_case?case=5480536480027070926&q=175+Ariz.+447+&hl=en&as_sdt=4,3